They like understanding that when they need their insurance, they will not need to develop a large amount of cash prior to their strategy begins assisting with the expense. So they 'd rather have a higher premium, however a lower deductible. It makes your costs more predictable.

A medical insurance premium is a regular monthly fee paid to an insurance provider or health strategy to offer health protection. The scope of the coverage itself (i. e., the amount that it pays and the quantity that you spend for health-related services such as physician check outs, hospitalizations, prescriptions, and medications) varies considerably from one health insurance to another, and there's often a correlation in between the premium and the scope of the protection.

ERproductions Ltd/ Blend Images/ Getty Images In other words, the premium is the payment that you make to your health insurance coverage company that keeps coverage totally active; it's the quantity you pay to buy your coverage. The Premium payments have a due date plus a grace duration. If a premium is not completely paid by the end of the grace duration, the medical insurance business may suspend or cancel the protection.

These are quantities that you pay when you require medical treatment. If you don't require any treatment, you will not pay a deductible, copays, or coinsurance. But you need to pay your premium on a monthly basis, no matter whether you use your health insurance or not. If you receive healthcare coverage through your task, your employer will generally pay some or all of the regular monthly premium.

They will then cover the rest of the premium. According to the Kaiser Household Structure's 2019 company benefits survey, employers paid an average of nearly 83% of single workers' total premiums, and approximately nearly 71% of the overall family premiums for employees who add household members to the plan.

The smart Trick of When Does Car Insurance Go Down That Nobody is Talking About

Nevertheless, considering that 2014, the Affordable Care Act (ACA) has actually offered superior tax credits (aids) that are readily available to people who acquire specific protection through the exchange. In order to be qualified for the premium aids, your income can't go beyond 400% of the federal poverty line, and you can't have access to cost effective, thorough coverage from your employer or your spouse's company - what does no fault insurance mean.

Let's say that you have been investigating healthcare rates and https://rocketreach.co/wesley-financial-group-email-format_b5a30097f67734a2 strategies in order to discover a strategy that is economical and ideal for you and your enjoyed ones - when is open enrollment for insurance. After much research, you eventually wind up selecting a particular strategy that costs $400 monthly. That $400 monthly cost is your medical insurance premium.

If you are paying your premium on your own, your regular monthly bill will come straight to you. If your company uses a group health insurance coverage plan, the premiums will be paid to the insurance plan by your employer, although a portion of the total premium will likely be collected from each staff member through payroll reduction (most large companies are self-insured, which implies they cover their workers' medical costs straight, normally contracting with an insurance provider only to administer the strategy).

The staying balance of the premium will be invoiced to you, and you'll have to pay your share in order to keep your protection in force. Alternatively, you can pick to pay the total of the premium yourself every month and claim your overall premium aid on your tax return the following spring.

If you take the subsidy upfront, you'll have to reconcile it on your tax return utilizing the very same kind that's used to declare the subsidy by people who paid complete rate throughout the year ). Premiums are set charges that need to be paid monthly. If your premiums are up to date, you are guaranteed.

The smart Trick of How Much Does Flood Insurance Cost That Nobody is Discussing

Deductibles, according to Health care. gov, are "the quantity you pay for covered health care services before your insurance plan starts to pay." But it is very important to comprehend that some services can be totally or partly covered prior to you satisfy the deductible, depending upon how the strategy is developed. ACA-compliant plans, consisting of employer-sponsored strategies and private market plans, cover particular preventive services at no cost to the enrollee, even if the deductible has actually not been satisfied.

Rather of having the enrollee pay the full cost of these gos to, the insurance strategy might need the member to only pay a copay, with the health strategy getting the remainder of the expense. But other health insurance are designed so that all servicesother than the mandated preventive care benefitsare applied towards the deductible and the health plan does not start to spend for any of them until after the deductible is met.

Even if your medical insurance policy has low or no deductibles, you will probably be asked to pay a relatively low cost for healthcare. This cost is called a copayment, or copay for short, and it will generally vary depending on the specific medical service and https://wesleyfinancialgroupscholarship.com/ the details of the individual's strategy. how does health insurance deductible work.

Some plans have copays that only apply after a deductible has been satisfied; this is increasingly common for prescription benefits. Copayments may be higher if month-to-month premiums are lower. Healthcare.gov describes coinsurance as follows: "the portion of costs of a covered healthcare service you pay (20%, for instance) after you've paid your deductible.

If you've paid your deductible, you pay 20% of $100, or $20." Coinsurance usually uses to the exact same services that would have counted towards the deductible before it was fulfilled. To put it simply, services that are subject to the deductible will go through coinsurance after the deductible is met, whereas services that are subject to a copay will normally continue to be subject to a copay.

The How Do Health Insurance Deductibles Work Ideas

The yearly out-of-pocket maximum is the highest total quantity a medical insurance company needs a client to pay themselves towards the general cost of their health care (in basic, the out-of-pocket maximum only uses to in-network treatment for covered, medically-necessary care in which any prior authorization guidelines are followed). Once a client's deductibles, copayments, and coinsurance paid for a specific year include up to the out-of-pocket optimum, the client's cost-sharing requirements are then finished for that specific year.

So if your health plan has 80/20 coinsurance (meaning the insurance coverage pays 80% after you've met your deductible and you pay 20%), that doesn't imply that you pay 20% of the total charges you sustain. It indicates you pay 20% till you strike your out-of-pocket optimum, and then your insurance coverage will start to pay 100% of covered charges.

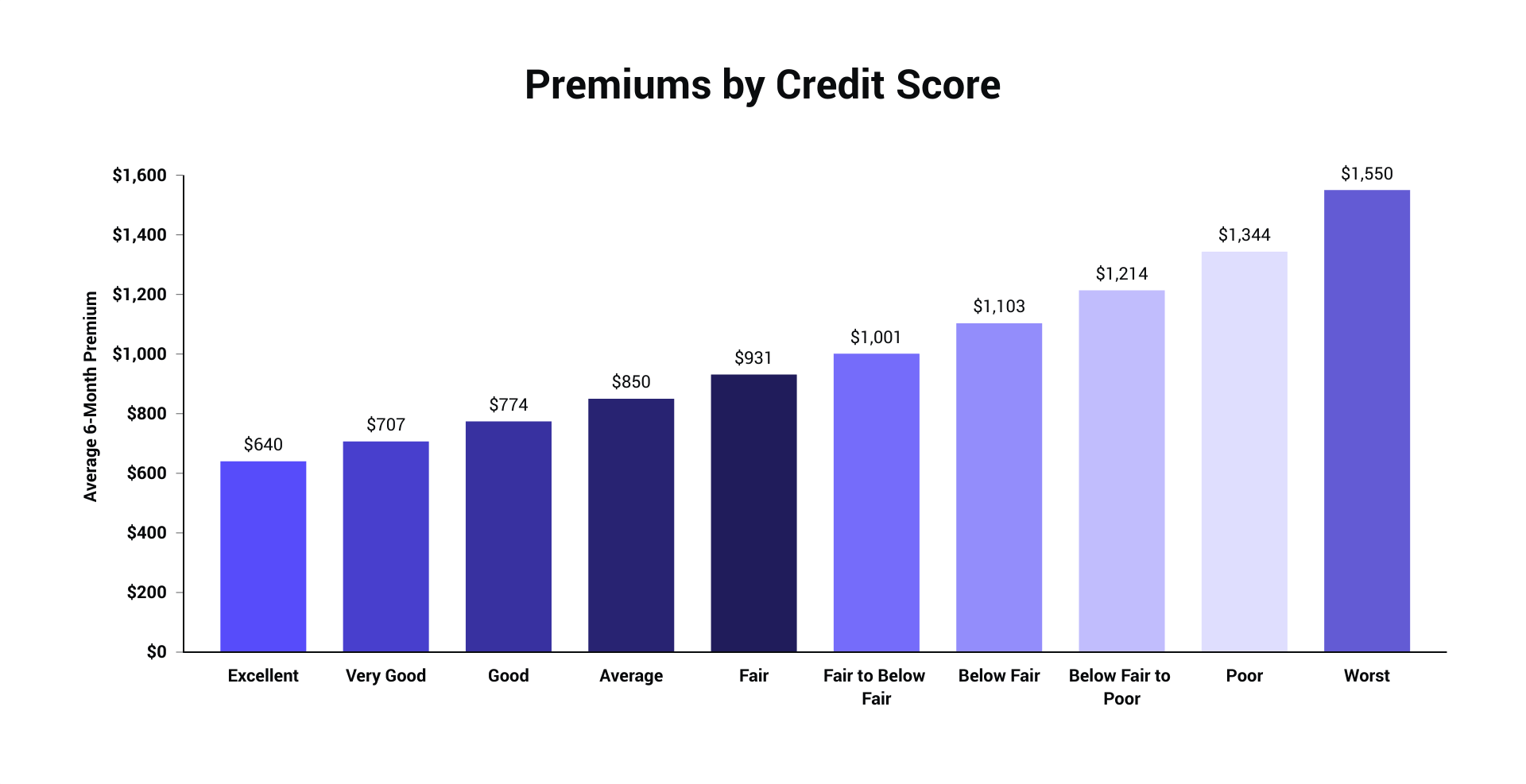

Insurance coverage premium is a defined amount stipulated by the insurance coverage business, which the insured person ought to occasionally pay to preserve the actual coverage of insurance coverage. As a procedure, insurance companies examine the type of coverage, the possibility of a claim being made, the area where the insurance policy holder lives, his employment, his habits (smoking for example), his medical condition (diabetes, heart ailments) amongst other factors.

The higher the risk associated with an occasion/ claim, the more expensive the insurance coverage premium will be. Insurer use insurance policy holders a variety of options when it pertains to paying insurance premium. Policyholders can typically pay the insurance coverage premium in installments, for example regular monthly or semi-annual payments, or they can even pay the entire quantity upfront before protection starts.